Close the Window on Cheque Fraud

May 6, 2019

With 734 million cheques processed in Canada in 2018, exposure to potential cheque fraud remains extremely high. I used to joke with my clients and say that the only way to effectively avoid cheque fraud was to not write any cheques, however given this is one of the oldest payment forms for business use, the legacy system continues to dominate in the B2B payment space.

Given the inability to eliminate cheques from your business payment system, here are a few simple tips to help reduce your exposure to potential cheque fraud:

1) Keep in mind that a completed cheque provides all the information necessary for a fraudster to access your bank account – financial institution, bank account number, cheque serial number sequence, sample layout and color of your cheque, and a sample signing officer’s signature.

2) By intercepting your cheque, fraudsters can access all the information they need. Cheques can be intercepted from your mail room, an employee’s desk, through Canada Post, or at the destination office. Keep completed cheques secure until dispatched and ask your suppliers to do the same before and after depositing.

3) While companies are typically good at protecting unused cheque stock, they tend to overlook any security for completed cheques. Even cancelled cheques are a source of information for criminals. Now with cheque imaged deposits, you are responsible for storing information for other companies who have provided you with cheques, before destruction after the holding period.

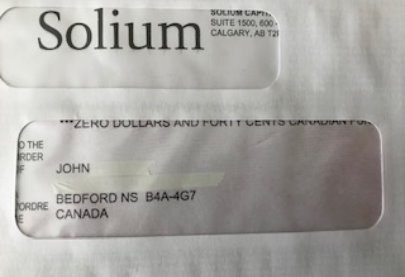

4) We have all received envelops in the mail with a clear window for the addressee. While these may make the mailing process easier for the sender, when there is a cheque used for the address, it is clearly visible and anyone handling the envelop (from your desk to the, hopefully, intended recipient) can easily see there is a cheque inside. As this is one matter that is 100% in your control, my advice to you is to eliminate the use of window envelops!

While these considerations are by no means an exhaustive list, they can provide some discussion points for you to consider when updating internal controls.